The Topic of the Month

Containers Shipping Rates Remain Extremely Elevated in 2022

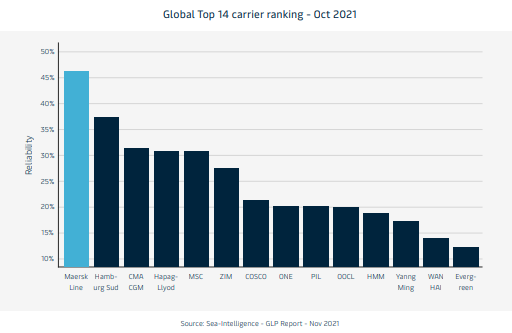

According to Maersk, the world’s largest shipping company, global ocean-based freight shipping would grow by 7% to 9% this year, a percentage point more than previously expected. Global supply networks have been thrown into turmoil as shippers attempt to fulfill growing consumer demand while simultaneously coping with port interruptions caused by Covid New Variant (omicron) outbreaks. According to IHS Markit, the dry bulk and container market balance will likely remain stable in 2022, but freight rates may need to be altered as vaccines reduce pandemic implications.

Ocean Freight Market Updates December 2021 United Arab Emirates

Outbound Ocean

Keys

| Sign | Meaning |

| ++ | Strong Increase |

| + | Moderate Increase |

| = | No Changes |

| – | Moderate Decline |

| — | Strong Decline |

ME – North America

One line Status: Congestion at the ports of Los Angeles/Long Beach and Savannah remains severe, while recent weather events have created difficulties in Vancouver. With a tighter capacity forecast on TPEB, demand remained steady. Due to congestion-related delays, sliding schedules, and carrier vessel recovery procedures, around 15% of capacity in December may be deemed effectively unavailable. Carriers are refusing to provide reservations for the United States East Coast due to transshipment port constraints. (DHL/Flexport)

Local Rates – Rates continue to increase. PSS/GRI applied by all carriers. (+)

Local Space – Critical (-)

Local Capacity/Equipment – Limited but available on selected carrier (-)

Notes: Bookings need to be placed 3-4 weeks in advance.

ME – Europe

One line Status: Carriers are overstressed and are restricting booking acceptance or rolling shipments. Schedule dependability is extremely low due to continual vessel delays and shifts. Space and equipment shortages persist as market demand constantly outstrips supply, with rates being extremely high for an extended length of time. Blank sailings and a lack of equipment worsen the overall space dilemma. (Flexport)

Local Rates – Rates remain at an all-time high. They have, however, remained constant throughout October and November 2021. Some slight increases are expected for December in the lead-up to the Chinese New Year period and due to blank sailing schedules. (+)

Local Space – Critical (-)

Local CapacityEquipment – Available (-/=)

Notes: Take advance planning for a month

ME – Africa

One line status – Rates, GRI, and premium surcharges continue to rise in West and South Africa. Only bookings made at least 2-3 weeks in advance will be considered. Carriers are releasing bookings against “Sea Priority/Shipping Guarantee” on the majority of routes, particularly the 20′. Carriers’ allotment for outgoing flights from the GCC is still restricted. While in East Africa, the space situation remains precarious. Only bookings made at least 2-3 weeks in advance will be considered. Carriers releasing reservations based on “Sea Priority/Shipping Guarantee”

Local Rates – Prices are on a general increase (+)

Local Space – Critical and low for East Africa, while relevantly at ease for West Africa (-)

Local Capacity/Equipment – available (+)

Notes – Only bookings made at least 3-4 weeks in advance will be considered and Priority is given to cargo utilizing “Shipping Guarantee” cargo

ME- Mediterranean MED

One line Status –Rates are still increasing. Space only available for booking 2-3 weeks in advance Lightweight cargo is preferred by carriers.

Local Rates – Prices are on a general increase (+)

Local Space – Limited but at a premium (-)

Local Capacity/ Equipment – Available

ME – ISC (Intra-Gulf)

One line Status — 20′ equipment is in short supply. Rates climbed in November 2021 and are expected to rise higher. There is less free time at the destination.

Local Rates – Price is on a general increase (+)

Local space – available (-/=)

Local capacity/ Equipment – available

Notes – Reservations must be made 2-3 weeks ahead to secure

ME – Far East Asia

One line status– Rates have increased, although there is a lack of equipment for Asia-bound freight. To save turnaround time, carriers prefer to relocate empty boxes rather than laden boxes. Reduced free time at the destination.

Local Rates – Price is on a general increase (+)

Local Space – Limited Space (-)

Local Capacity/Equipment – available (-/=)

Notes – Reservations must be made 2-3 weeks ahead to secure

ME – China

One line status – In the fourth quarter of 2021, Christmas and Chinese New Year will boost strong demand for container transportation in China. Costs have risen due to a shortage of equipment for items destined for Asia. While electricity shortages in some Chinese areas may limit output, demand remains exceptionally strong.

Local Rates – Price are on a general increase (++)

Local Space – Tight Space (-)

Local Capacity/Equipment – available (-/=)

Notes- Reservations must be made 2-3 weeks ahead to secure

ME – Oceanic

One line status- Congestion at South East Asian transshipment ports is causing transit delays of several weeks. The monthly capacity and spot rate remain constant. There is a significant probability that space will be available if bookings are made in advance.

Local Rates – (+)

Local Space – (-)

Local Capacity/Equipment – (–)

Notes – Reservations must be made at least 4 weeks ahead to secure

ME – Latin America

One line status – Due to insufficient capacity, most carriers are not taking bookings. The situation is expected to remain unchanged in the near future.

Local Rates– Prices are on a general increase (++)

Local Space – Very tight (–)

Local Capacity/Equipment – Available (-/=)

Notes- Reservations must be made at least 4 weeks ahead to secure

Inbound Ocean market update for the United Arab Emirates

North America

One line status- After a year of month-over-month hikes, rates are beginning to level out in December. As a result of the carriers’ financial success, new services and service simplification have been implemented. Due to congestion concerns, the Port of Savannah has been shifted to Charleston. The current situation is projected to last till the end of the year.

In addition to void sailings and delays, deteriorating schedule integrity poses substantial issues with announced earliest return dates and vessel cut-offs at the port. (DHL)

Local Rates – Rates are stabilizing for December after a full year of MoM increases. (+/=)

Local Space – Tight from the US West Coast. The US East Coast is showing signs of improvements in available spaces. In the US Gulf space has increased with capacity more readily available (-/=)

Local Capacity/Equipment – Deficits on containers and chassis are still plaguing IPI origins. Availability for standard equipment at ports has not been an issue, but any special equipment is hard to come by. (=)

Notes – Place bookings 4 to 6 weeks in advance to secure your equipment, trucking and vessel space.

AsiaPacific

One line Status –Vessel delays are still widespread, resulting in a variety of vessel slides. Delays in transshipment ports have been recorded to last up to 2-3 weeks. The market is still quite robust, but markets in the Middle East and Africa are exhibiting indications of waning.

Local Rates – increase (+)

Local Space – Critical (-)

Local Capacity/Equipment – Under capacity (-)

Notes- Book 2-3 week before, Trucking shortage

Europe

One line status – Rates may be slightly reduced based on the service and alliance.

Local Rates – Rate slight increase (+/=)

Local Space- Critical (-/=)

Local Capacity/Equipment– (=)

Notes- Book 2-3 week before

Latin America

One line status –The region has been plagued by structural service modifications and local labour activities. In 2022, no new capacity is projected to enter the market. Africa’s rates are rising as a result of a lack of services.

Local Rates – Rate increase (+)

Local Space – Critical (-)

Local Capacity/Equipment – (-)

Notes- Book 2-3 weeks before

Indian SubContinent (ISC)

One line status- Empty equipment and uneven or blanked sailing schedules will continue to be an issue for ISC exporters in the near future.

Local Rates– Rate increase (+)

Local Space- Critical (-/=)

Local Capacity/Equipment – Limited (-)

Notes- Book 2 weeks ago

Air Freight Market Updates December 2021 for the United Arab Emirates

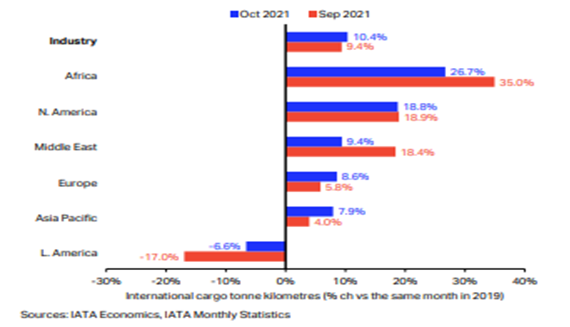

Air Freight Demand – Global demand, measured in cargo tonne-kilometers (CTKs), increased 9.4 percent over October 2019. IATA provided October 2021 statistics for global air cargo markets, indicating that demand remained substantially above pre-crisis levels and that capacity restrictions have improved marginally. The discovery of a new variant (Omicorn) of concern in South Africa prompted governments to tighten international travel restrictions in order to gain time and prevent the spread of the Omicron variant.

Carrier Capacity – Capacity issues were gradually being resolved as more passenger travel meant more belly capacity for air freight. Concerns have been raised about the implications of government reactions to the Omicron varient. If it reduces travel demand, capacity issues would worsen. After over two years of COVID-19, countries now have the experience and tools to make better data-driven choices than the primarily knee-jerk reactions to travel restrictions witnessed to date.

Local Rates – Airlines continue to aggressively control yields; excess capacity is still available at a charge. Rates were +86% higher on August 21 than the 2019 baseline and +20% more than a higher 2020 baseline. Rates will stay high as we continue to see massive demand growth versus limited capacity. Rates to/from Asia Pacific (particularly China) are anticipated to continue high owing to persistent limitations; market rates are roughly four times higher than average.

The Middle East and Air Carriers ME

When compared to 2019, international CTKs growth for Middle East carriers fell sharply, from 18.4 percent in September to 9.4 percent in October. This was caused by traffic problems on numerous critical routes, including the Middle East-Asia and the Middle East-North America.- IATA

African airlines increased international cargo volumes by 26.7 percent in October, a decrease from the previous month’s (35%), but still the highest gain of any region. International capacity was 9.4 percent greater than pre-crisis levels, with the Middle East being the only area in positive territory, albeit on a minor scale.

Asia

In SouthEast Asia, export demand is steadily rising, and warehouse terminals are overloaded with cargo. Bookings should be made at least 1 to 2 weeks in advance to ensure the greatest possible availability. Flight cancellations for the Christmas and New Year’s holidays have yet to be announced by airlines. Due to limited capacity, ex-BKK airlines can only take modest shipments. We recommend making reservations at least 10 days before the CRD.

Space is limited in ex-Northern Vietnam, and demand is surging. Flight cancellations are usually announced around this time, although official news is still forthcoming. The rates for FEWB lanes have been raised.

Through mid-December in Taiwan, capacity to the US East Coast is nearly fully booked. Rate hikes for US east coast and SFO lanes are expected due to sustained strong demand and will likely be effective from December 6 through mid-month, although official announcements are awaited.

The market position outside of South China remained unchanged from the previous week. Capacity is limited since some PAX flights continue to be cancelled. The rates for both TPEB and FEWB lanes have increased, particularly for FEWB.

In North China, demand is rising again, and rates have gone up from the previous week. The advent of the South African Omicron form of Covid is anticipated to further complicate the global supply chain. The market is expected to remain tight until the Lunar New Year. Covid-related freight to the EU is quickly increased and is likely to be the primary driver of the FEWB trade route.

Europe

Capacity on the Transatlantic trade channel has been reintroduced; yet, demand continues to exceed capacity, causing tariffs to increase week over week. There is more ocean-to-air conversions on the market from the EU to the US, as shippers seek the quickness of air options to replace stock levels before Christmas.

Congestion in AMS airport terminals has been reduced, however, congestion at other European hubs remains a barrier. It is projected to persist till the end of the year and will have a detrimental influence on the transit times of all freight forwarders. Handlers are hiring more workers and constructing new warehouses when space is available. Additional terminal entrances and exits are being created in order to free up space for additional vehicles to pick up or drop off cargo.

When compared to pre-crisis levels, international CTKs growth for European airlines increased from 5.8 percent in September to 8.6 percent in October. Manufacturing activity is resilient but decreasing, and inflation is rising, albeit at a slower rate than in the United States. International capacity was down 7.4 percent compared to pre-crisis levels, a notable improvement from the previous month when it was down 12.8 percent. In October 2021, European carriers witnessed an 8.6 percent rise in international cargo volumes compared to the same month in 2019, an improvement over the previous month (5.8 percent ). Manufacturing activity, orders, and lengthy supplier delivery periods continue to favour air freight demand.

North America & Latin America

The ban on EU travellers has been lifted by US officials, and European airlines are gradually increasing belly hold capacity. LATAM has also received more capacity. In November, US export demand increased even further. Larger shipments from large outbound gateways can take 2 to 4 days from the time they are booked to uplift into the EU, LATAM, or Asia. Early reservations are advised.

LAX/ORD/JFK Ground handlers are still experiencing backlogs and are utilizing off-airport facilities to manage the influx of inbound goods, which has a knock-on impact on the export side. To accommodate lengthier throughput times and screening requirements, many have reduced their free storage duration and imposed new, earlier close-outs for exports.

Rates from the United States to LATAM and several Asian destinations remain high. Rates entering Europe have not changed significantly. Fuel surcharges have gone up. Due to the present labour scarcity, top European hubs have somewhat longer transit times and a high throughput time.